Crypto Market Making Fund - 03 May Report

· 2026-06-03 10:41:59

Market Making Fund Strategy Performance Report – May 2026

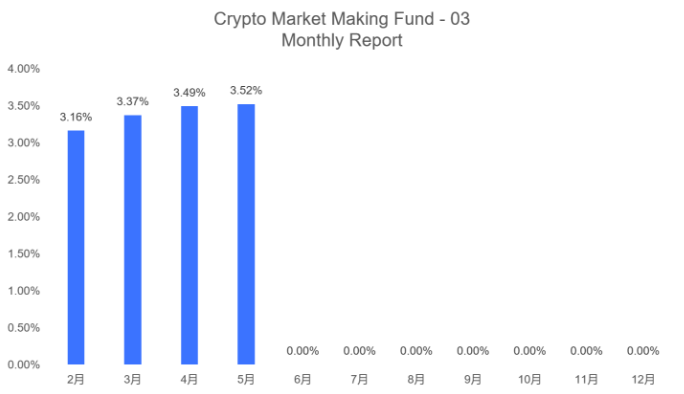

Monthly Fund Return: +3.52%

I. May Crypto Market Review

The cryptocurrency market in May 2026 was characterized by range-bound consolidation, fierce long-short contention and divergent capital flows. Such sideways trading created favorable conditions for steady market making revenue throughout the month.

1. Major Cryptocurrency Performance

Bitcoin traded repeatedly within the $75,000–$83,000 range, testing the $80,000 resistance multiple times without a decisive breakout; its monthly high stood at $85,900 and low at $72,600 with intraday swings frequently hitting hundreds of US dollars. Ethereum remained under pressure in a tight band of $1,980–$2,250, lacking any sustained directional trend.

The Crypto Fear & Greed Index lingered at 28 (Extreme Fear) for most of the month amid panic retail sell-offs, while spot Bitcoin ETFs registered persistent inflows as institutional investors accumulated positions on dips, forming a structural divergence between retail panic and institutional accumulation.

2. Trading Volume & Derivatives Landscape

Total market capitalization hovered around USD 2.65 trillion with stable average daily spot turnover. Perpetual swap funding rates alternated periodically between positive and negative. Altcoins showed polarized performance: leading public-chain and RWA tokens maintained solid liquidity, whereas small-cap meme coins saw spiky price swings and intermittent liquidity dry-ups.

Progress on U.S. crypto legislation at month-end fueled shifting regulatory optimism, amplifying short-term volatility and widening spread opportunities for market makers.

3. Market Summary

No prolonged bull or bear trend emerged; range consolidation plus intermittent spike volatility defined May’s market structure. Such choppy conditions were optimal for passive limit-order market making and cross-exchange arbitrage, matching the fund’s conservative market-making framework.

II. Core Market-Making Strategies & Return Breakdown

The fund delivered an overall monthly return of 3.52%, broken down as: spot order-book spread income 2.11%, cross-exchange spot-futures arbitrage 0.87%, neutral grid market making on derivatives 0.54%. The portfolio adopted tiered market making, multi-strategy allocation and dynamic position sizing tailored to range-bound markets.

1. Passive Maker Order Market Making on Major Spot Coins (Primary Return Driver)

Tiered limit orders were deployed to fit BTC and ETH’s established trading ranges:

1. Core trading bands were set at BTC [$73,000, $84,000] and ETH [$2,000, $2,230]. Five tiers of evenly spaced bid/ask limit orders were placed to capture natural order-book spreads plus exchange maker rebates; recurring range rotation generated core earnings.

2. Dynamic spread calibration: bid-ask spreads were moderately widened during panic sell-offs and thinning order-book depth, and tightened amid mild rebounds and ample liquidity to boost fill rates.

3. Position control: single-currency spot exposure capped at 18% of AUM to mitigate unrealized losses from decisive range breakdowns.

This strategy contributed 60% of monthly profit and was the key driver of net asset value growth.

2. Neutral Spot-Futures Arbitrage & Perpetual Funding Rate Arbitrage

Leveraging cyclical swings in perpetual swap funding rates:

1. When perpetual contracts traded at steep premiums with positive funding (longs pay shorts), paired long spot + short perpetual positions to lock in steady funding proceeds; positions were reversed during deep futures discounts with negative funding to capture risk-free rate spreads.

2. Cross-platform spread arbitrage: automated micro-blotter trading captured fleeting price discrepancies between CEX and DEX listings, accumulating small per-trade profits at high frequency while hedging underlying spot inventory volatility.

3. Neutral Grid Market Making on Mid-to-Large Cap Derivatives

We selected liquid leading public-chain and RWA tokens for two-way neutral grid deployment: short orders triggered on upward price moves and long orders on declines, with profit booked on range oscillations without directional speculation. Small-cap low-liquidity tokens were traded with minimal allocation and strict leverage constraints to avoid flash-crash liquidation risks.

4. Dynamic Risk Control Framework (Profit Preservation)

1. Breakdown risk management: all new maker orders suspended and market-making exposure cut to 30% of baseline upon decisive downside breaks below key supports (BTC < $72,500 / ETH < $1,980); position trimming also activated on decisive upside breakouts to reduce directional drawdowns.

2. Capital segmentation: 70% allocated to spot core holdings and regular market making, 20% for derivatives arbitrage, 10% held in stablecoins for emergency liquidity replenishment or risk avoidance during market shocks.

3. Black-swan contingency: all derivative exposure closed with one-click execution and rapid spot de-risking upon abrupt negative regulatory news or large-scale market dumps.

III. Monthly Strengths & Existing Drawbacks

Advantages

1. Strategy was well-aligned with May’s sideways market; directional speculation was discarded in favor of spread harvesting, delivering consistent outperformance versus most directional long/short funds.

2. Multi-strategy diversification created complementary returns across spot and derivatives, insulating overall NAV from single-token price shocks.

Deficiencies

1. Mild late-month market breakdown triggered temporary unrealized losses on core spot holdings, partially eroding arbitrage gains.

2. Occasional liquidity exhaustion in niche-sector tokens left some grid orders unfilled, dragging down marginal capital efficiency.

IV. June Market Outlook & Strategy Optimization Plan

1. Forward Market Outlook

June is highly likely to continue May’s weak consolidation pattern. Fed liquidity shifts and pending U.S. crypto regulatory rulings will remain headline catalysts. BTC is expected to rotate into a new $70,000–$80,000 trading band with moderately elevated volatility; sustained directional moves remain unlikely. Market-making fundamentals stay favorable with heightened downside risks vs May.

2. Optimized Market-Making Roadmap

1. Reduce core spot inventory: single-major spot cap lowered from 18% to 12% of AUM; stablecoin reserve raised to 15% to cushion losses from range breakdowns.

2. Dynamic spread expansion: widen quoted order-book spreads amid rising volatility to cut unprofitable over-fills and prioritize guaranteed spread returns.

3. Expand compliant RWA market-making pool: launch dedicated maker pools for top-tier regulated RWA tokens amid ongoing traditional financial institutional inflows to reduce concentration risk on BTC & ETH.

4. Revised grid parameters: cut per-tranche leverage on derivative grids and narrow grid spacing; shift toward defensive reverse grids to adapt to June’s biased-downward range trend.

V. Monthly Conclusion

Benefiting from May’s range-bound market-making environment, the fund posted a robust +3.52% return via the combination of passive order-book making, spot-futures arbitrage and neutral grid trading, validating the quantitative market-making model’s efficacy in sideways markets.

With rising risk aversion and elevated downside risks in June, the overall strategy shifts from balanced market making to defensive conservative positioning via reduced risk exposure and enlarged cash reserves, continuing to earn stable spread income from market volatility.